Greetings,

Interim Earnings Season

The majority of companies have now reported their interim earnings, with only the smaller ones having a few more days to lodge results before the end of February.

There was a significant increase in volatility in share prices on the day of individual earnings announcements, partly driven by automated trading utilising artificial intelligence and natural language processing. In many cases, this reversed over the next few trading days, particularly when short positions were covered.

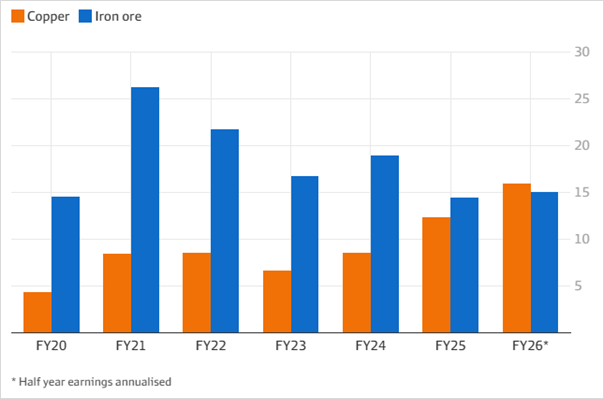

The major banks performed very well, in some cases reaching new all-time highs, as did the resources sector, where the bellwether BHP also hit new highs based on the increased price of copper as an alternative to its reliance on iron ore.

BHP earning by resource ($USb)

Source: BHP ASX Filings

In contrast, many growth stocks, particularly in healthcare, struggled and declined significantly, with Cochlear and CSL being the most pronounced. Technology stocks such as Xero and WiseTech also fell significantly, primarily over fears that AI would lead to alternative, cheaper services that might replace their dominant market positions.

This is another stark reminder of why it is important to diversify across a portfolio and not be overly reliant on one or two individual shares.

Importantly, the actual dividends due to be paid out remain strong, reflecting the strength of the financial services sector, which is benefiting from significant efficiency gains from improved technology while maintaining and returning reasonable earnings.

The wider macro issues of poor productivity across the workforce remain an area of major concern and are ultimately a handbrake on the stock market continuing to reach new highs.

Global Tensions

At the time of writing this newsletter, it appears that the US may be close to an imminent attack on Iran, which could have a profound effect on the short-term movement of shares in general, and anything linked to oil more specifically.

While we have been through similar situations in the past and markets have gone on to recover, it is simply common sense to be particularly prudent at this time and wait to see how this plays out.

Strong global economies are the highest priority for Western governments, and if there is a period of turmoil, they are likely to reduce interest rates as an automatic economic stabiliser.

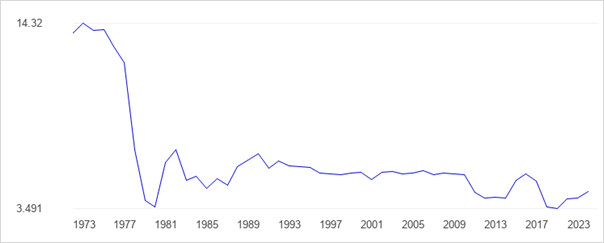

Those of you with long memories will remember the oil shocks in the late 1970s, although Iran’s share of global oil production has fallen substantially in recent years to 4.4%.

Iran: Percentage of World Oil Production

Source: theglobaleconomy.com

International Shares

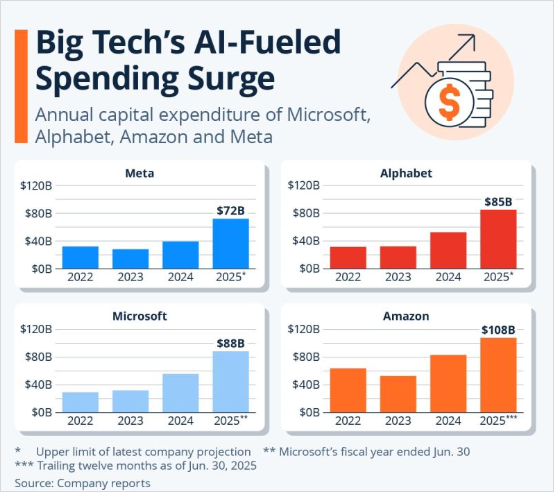

As expected, we are beginning to see some rotation in the US from companies manufacturing AI to those actually utilising it to run better businesses.

There are genuine concerns that the larger AI producers are over-investing in future data centre capacity (including Amazon, Nvidia, Microsoft, Google and Meta), and perhaps they would be better served if there were one principal provider with much of these costs shared.

Looking back through business history, including the railroads of the 19th century in the US, there have been times when oversupply led to very significant losses as competing companies sought to become the leader in their market at all costs.

It is fair to say that the major technology companies are now priced for perfection, and any underperformance in their quarterly earnings may be severely punished. To some extent, this has been reflected in fund managers specialising in this area, whose monthly performance has been very volatile.

The best outcome would be for efficiency gains to be widely spread throughout businesses, leading to an improvement in wider operating margins, similar to the development of computer technology in the 1990s.

Source: Statista

Stabilising Returns

Against this backdrop, it is essential that a growing proportion of client returns comes from less volatile settings.

As discussed in previous newsletters, the growth of private equity and private credit – which are less correlated to listed stock markets – is becoming increasingly prevalent in client portfolios. While there can sometimes be liquidity constraints, this approach allows us to generate consistent monthly income without the gyrations of the stock market.

This includes unlisted infrastructure and private equity investments seeking to generate strong returns from companies that do not wish to list on the ASX but would rather keep part of their businesses private.

Accordingly, where appropriate, we are increasing our allocation to this sector for clients at their annual review.

As investors, we retain a very long-term horizon, primarily looking to generate adequate income to cover living expenses through all market conditions. The growing application of advanced automated trading is leading a significant portion of the market to trade on very short-term information, creating greater volatility.

In Australia, it is now estimated that 30% of daily trade takes place between 4:00 and 4:10 pm during the end-of-day matching process.

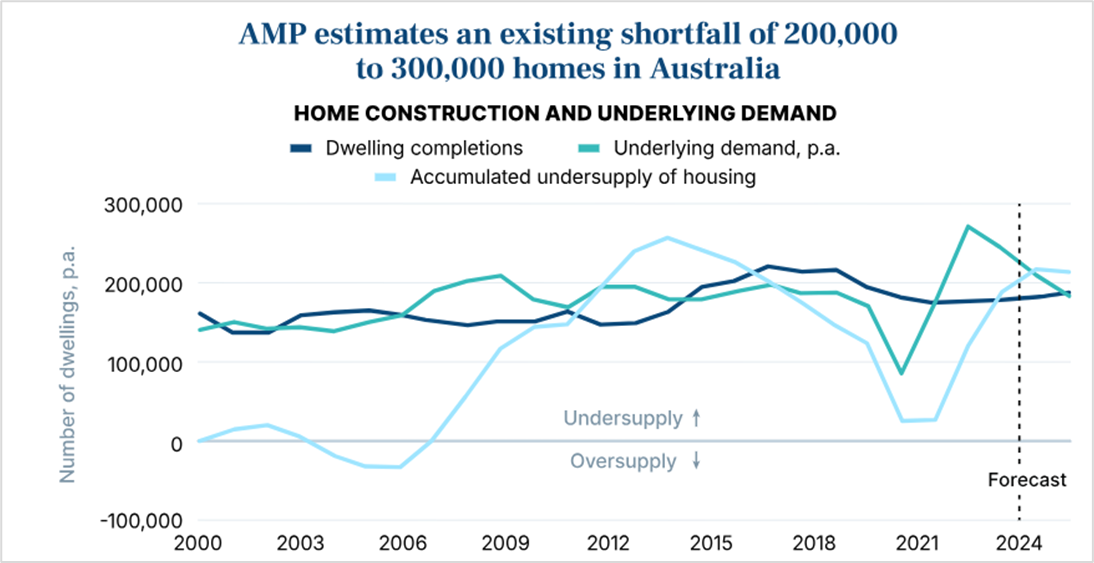

Australian Residential Property

While the RBA increased interest rates by 25 basis points earlier in the month – partially reversing the three reductions from last year – auction clearance rates remain strong, reflected in current property prices.

Many mortgage holders increased their effective repayments when interest rates fell last year and appear to be taking this in their stride. However, should interest rates rise further, there may well be a change in psychology and a slowdown, particularly in the investment side of property ownership.

More importantly, with very little movement on the supply side and net migration of at least 250,000 per year, it is difficult to conclude anything other than that property prices will continue to rise.

The Labor Government has floated a potential change to capital gains tax which, if introduced, would make investment properties less attractive, although existing properties would likely be grandfathered. We will gain a better understanding of this in the May Budget.

Australian Property Shortfall

Source: Australian Property Update

News

It is very much business as usual, with a steady stream of referred clients keeping us busy.

We are constantly looking at ways to improve our efficiency without diminishing the importance of our personal relationships with you. Cyber security and the overall ease of doing business with us remain absolutely top of mind.

Our goal is to provide a stable and reliable service in all market conditions, particularly during periods of change in clients’ lives.

There are some good investment opportunities being presented to us at the moment, which we will share with you once we are confident they meet your investment objectives in a prudent and appropriate manner.

Sincerely,

Tony and Fiona

ABN 42 060 673 814 • AFSL No. 407238