Greetings,

Fallout from the Federal Budget

Domestically, the main news has been the negative reaction to the recent federal budget, which appears destined to go through the Senate early in July, with an effective start date of 1 July 2027. This does give time for clients to plan ahead and, as part of this, we will need to revalue every asset – listed and unlisted – in Australia as at 30 June 2027, which is a mammoth job and will then become the cost base for CPI indexing in future years when calculating capital gains tax. The political motivation behind this is to tax personal exertion income and realised asset appreciation at the same rate, irrespective of the risk undertaken.

This indexation model would apply equally to both defensive listed assets and high-growth international shares, irrespective of the differing levels of risk associated with these investments. From a client behavioural point of view, it is more likely that Australian investors will focus on income-paying, fully franked dividend shares, as opposed to higher-growth global shares, where much of the potential for higher returns is currently coming from. This will also make it much harder for new Australian high-growth companies to list on the ASX, and many will choose to list overseas.

For existing assets, there will effectively be two components of CGT calculations: the component under the older system, which will still be based on the 50% discount, and a new indexed component from 1 July 2027. At the very least, this is going to create additional paperwork and, in my opinion, significantly distort investment decisions. For clients close to the top of a tax band, the CGT will be added to your taxable income, which may well take you into a higher tax bracket, compounding the problem.

There is a carve-out for the same assets held through superannuation, which will provide a greater incentive to keep growth-type investments within superannuation (which would be subject to a CGT of 10% in accumulation and zero at drawdown), as opposed to holding the same investment in your personal name and being taxed at your marginal rate, less any indexation.

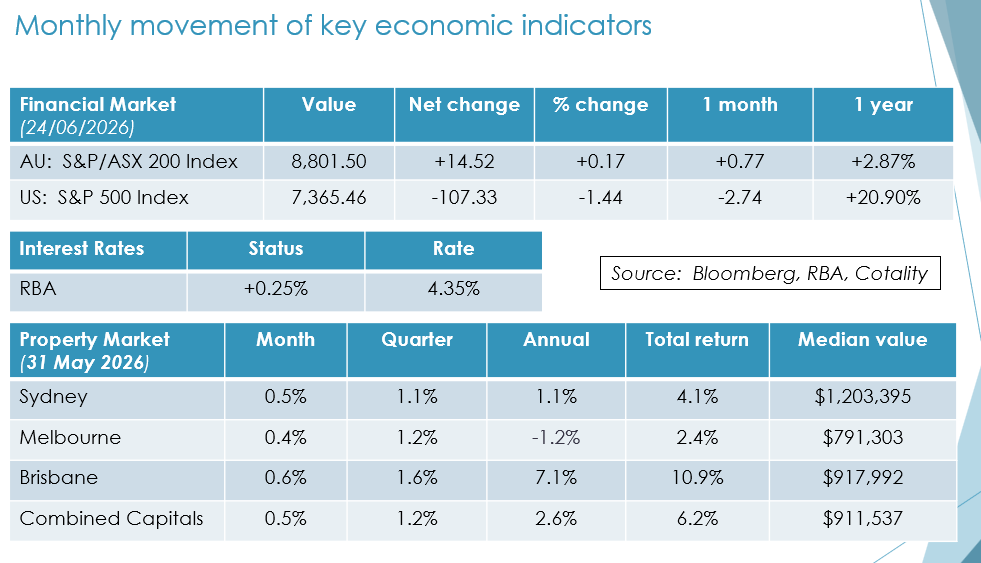

The fallout in the Australian residential property market was swift and brutal, with auction clearance rates in Sydney down to 40% (the lowest since COVID), and the effective freezing of the market until there is far greater clarity as to government longer-term policy, including whether these changes will be wound back either by the current government or at a future election. In the meantime, the RBA kept interest rates steady last week, and it is very unlikely that interest rates would be lifted given these circumstances. As a major employer, a significant downturn in residential property would severely impact GDP, not to mention the tax take for state governments from stamp duty.

Subject to financial capacity, there is still no limit on existing investors purchasing more properties, particularly if prices fall significantly. It is, in fact, first home buyers who have recently purchased on a 5% deposit who may now be underwater and are the most financially exposed, particularly if they have insecure work arrangements. Ultimately, property still remains a supply issue, and changing the incentive to purchase existing properties is really just tinkering at the edges.

So, I think in aggregate it is best to sit this out through the winter, stay cashed up, and wait for future signs—both political and economic—before making any significant investments. For those of you in the retirement phase, there should be very few changes, with your income streams remaining solid. It is the next generation that will really struggle to get ahead financially with these policy settings.

Federal Government Summary on Budget 2026-27 Negative Gearing and Capital Gains Tax Reform (Source: Australian Tax Office).

The Government has budgeted, through Treasury, that rents will increase by only $2 per week and that property values will fall by 2% from where they would otherwise have been. Both of these assumptions seem quite optimistic. If there is a shortage of buyers, it is entirely possible that the actual outcomes could be far more negative.

As mentioned previously, a similar situation occurred in New Zealand several years ago, which was later reversed. Likewise, the Keating Government in the 1980s reversed a decision on CGT. Ultimately, this will come down to the broader impact on the economy and employment.

There have also been several amendments to the original proposals, including increased exemptions for small businesses to receive CGT relief based on turnover. Additionally, as of this morning, SMSFs will no longer be able to take out new loans to purchase property, following a cross-party agreement between Labor and the Greens.

Global Equities

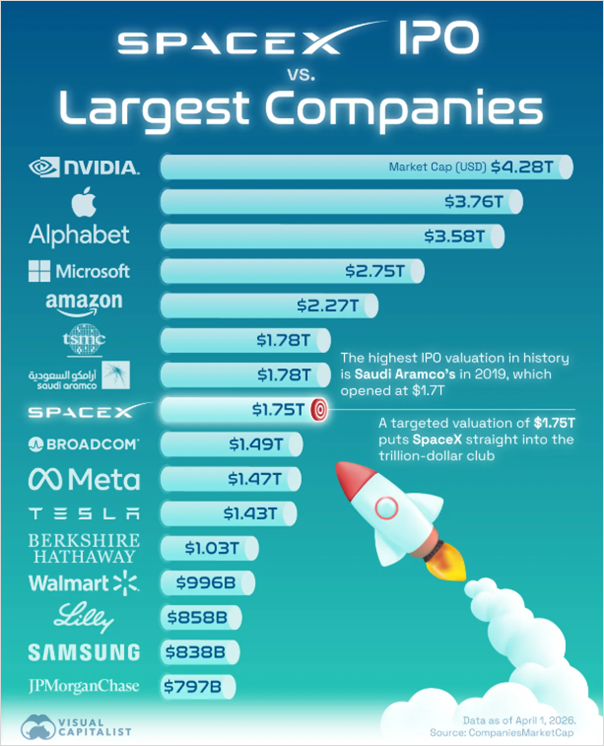

The major story in global markets has been the launch of SpaceX (Space Exploration Technologies Corporation; NASDAQ: SPCX) on the NASDAQ last week – the largest IPO in history and now the fifth-largest listed company in the world.

The share price traded strongly in the first few days but declined somewhat overnight due to profit-taking. It is worth noting that only around 4% of the company is publicly traded, which does distort the valuation. Investors are largely backing the vision and track record of Elon Musk, who is now reportedly the first person worth $1 trillion.

At this stage, we view this as a highly speculative investment. Access options include direct investment via platforms, space-focused ETFs, and listed managed funds with exposure to SpaceX, such as Pengana Private Equity Trust (PEI) and Hyperion Global Equity Trust (HYGG).

SpaceX IPO vs. Largest Companies

Source: Visual Capitalist, Companies Market Cap

Based on the current share price of SpaceX, it now has a very similar value to the entire Australian stock market.

SpaceX valuation compared with the Australian stock market

Source: ChatGPT

Hot on its heels are the expected IPOs of Anthropic (owner of Claude) and OpenAI in the coming weeks. Both are anticipated to be very substantial listings and heavily oversubscribed. Similar to SpaceX, access will likely be available through a number of channels for those interested in gaining exposure.

AI adoption is becoming widespread across businesses and is clearly improving efficiencies. However, there are valid concerns around misuse of automated communication, as well as potential impacts on employment and social cohesion.

More broadly, despite ongoing unrest in the Middle East and a fragile ceasefire, global equity markets remain strong. Much of portfolio growth is currently being driven by these markets. The largest US-listed companies are now significantly larger than the entire Australian economy, which is an important consideration when making investment decisions.

Companies can operate globally and target a worldwide addressable market, while Australia still represents only around 2% of global equity markets.

Australian Residential Property

As expected, given the disruption following the recent budget, auction clearance rates are at multi-decade lows and discretionary property purchases have largely paused.

In this environment, it is highly unlikely, in my view, that interest rates would be increased further. In fact, the four major banks are all forecasting rate cuts next year. We are likely entering a period of stagnation, potentially through to Christmas, until the full impact of the budget becomes clearer.

Looking at comparable markets such as the UK, US and Germany, it is also likely that the corporate build-to-rent sector will expand and partially replace individual investors who own one or two properties. In this model, large corporations develop residential complexes (e.g. 200 units), retain ownership, and lease them out.

Globally, this model has presented challenges, particularly where rent maximisation impacts affordability for lower-income tenants. Regardless, Australia must address the ongoing housing supply shortage to accommodate continued population growth.

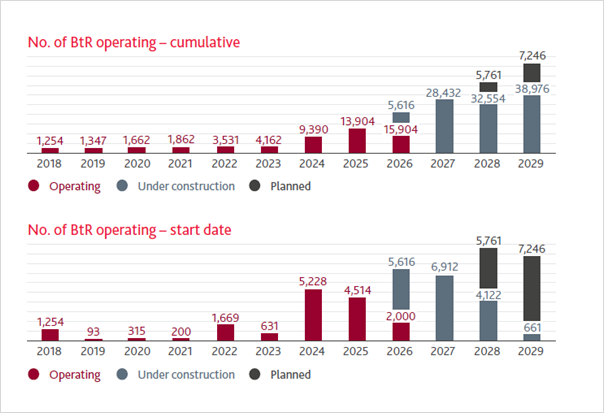

The graph below shows how the Build to Rent market is growing in Australia with companies building entire blocks of units, retaining ownership and leasing out apartments. This may well become the dominant method of renting in Australia as opposed to renting off mum and dad who own one or two negatively geared properties.

Australian Build to Rent Growth

Source: BDO Australia

Year-End Planning Checklist

- Top up super contributions up to $30,000 (where applicable).

- Consider realising capital losses to offset gains.

- Prepay upcoming expenses where possible.

- If running a business, consider purchasing assets up to $20,000 to claim an immediate deduction.

- Consider prepaying interest on investment loans.

- Review charitable giving opportunities.

We are here to help

This is one of the busiest times of the year for our firm, and we are keeping the office open extended hours to support you through financial year-end.

If you have any questions around tax planning, please send us an email and we will respond promptly. We greatly appreciate your continued support, referrals, and well wishes throughout the year.

Sincerely,

Tony and Fiona

ABN 42 060 673 814 • AFSL No. 407238