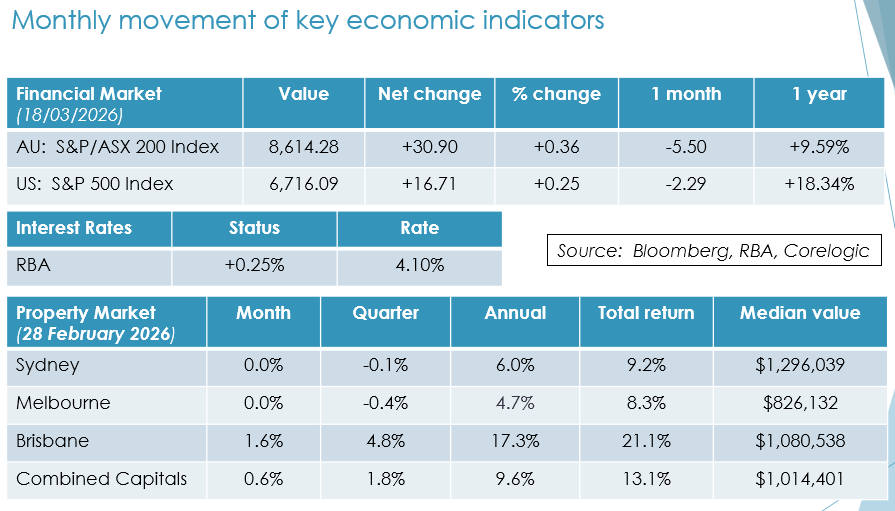

Greetings,

Obviously, news is dominated by the conflict in the Middle East, and I can confirm that all clients who were in the region are safe and accounted for. We have been through many wars over the years and, in general, it is best to retain adequate cash reserves to avoid any forced selling and impulse, emotional selling at a time of peak volatility. Outside of oil prices, the wider equity markets have been remarkably stable and have fallen by less than 5% from their all-time highs reached several weeks ago.

Economic impact on conflict in the Middle East

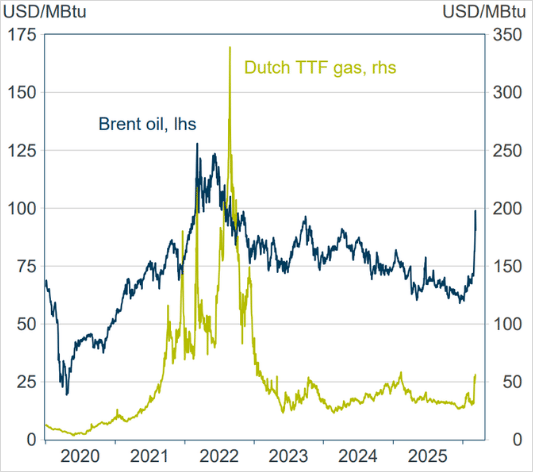

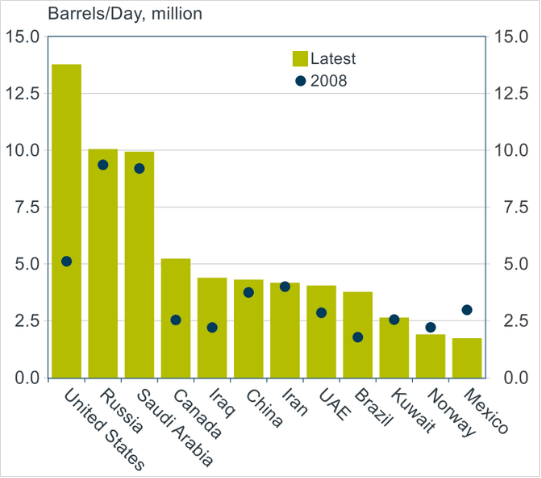

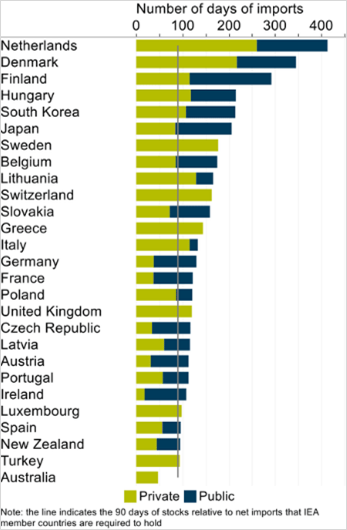

I think it is fair to say that this was a conflict that was expected and, to some extent, predicted by the market, and that if the US and Israel had not attacked there could have been a worse circumstance at a later stage should Iran use their reported 450 kilos of enriched uranium to make up to 11 nuclear bombs. After the initial attacks just over two weeks ago, markets have moved from their usual high level of volatility into more of a holding pattern, waiting to see what the final outcome will be in the resolution of this matter. The movement in the oil price was lower than at the commencement of the Ukraine war and was heavily driven by speculation as opposed to the actual need to use oil as a resource. The US remains the largest oil producer in the world, with Iran only accounting for 4%; however, the much-spoken-of Strait of Hormuz has a disproportionate effect on the wider global economy, including other essential products such as fertilisers. The International Energy Agency (IEA) has begun releasing some of the oil reserves, with at least 90 days’ stock being available for most countries. Sadly, Australia is an outlier, holding a much lower level of reserves, which is impacting our petrol prices based on concerns of a prolonged dispute. Overnight, two leaders of the Iranian regime were eliminated, and this may bring a faster conclusion to this conflict.

Oil and European gas prices

Source: Challenger, Macrobond, Bloomberg

Largest Oil Producers

Source: Challenger, Macrobond, EIA

National Oil Stockpiles

Source: Challenger, Macrobond, EIA

The first phase of this war seems to have concluded, and it really is just a case of what is planned for the future reconstruction of Iran and its 90 million population. Managed well, this could lead to improved harmony in the Middle East between all the neighbouring countries, leading to a period of greater prosperity and freedom from oppression. No doubt this is being war-gamed in both Washington and Jerusalem, as the key issue is finding future leadership of Iran that is sustainable, and avoiding some of the problems that were encountered in Iraq and Afghanistan some 20 years ago. A possibility is the Shah’s son, now living in the US, who has proposed heading up an interim government prior to free and fair elections. In the meantime, many of the Ayatollahs have left Iran, with their money now moving over to Britain and Canada, and even possibly Australia.

Australian Interest Rate Decision

In a line-ball decision 5/4, the RBA voted to increase interest rates to 4.1%, partly driven by increased fuel prices from the Middle East conflict, but primarily by excess domestic government spending. The decision was based on the fact that expenses continue to grow, especially in the federal government sector, at twice that of productivity for the quarter to December 2025. In the private sector, there have been a number of reductions in headcount at the major banks and technology companies such as WiseTech and Atlassian. However, similar action has not been taken in the public sector. While there is much talk at the moment about intergenerational fairness, the best thing we can do for our next generation is to ensure that we do not have excessive debt based on poor management in our time. The four major banks passed on these increases immediately, and the overall effect should be to reduce the demand for debt. Interestingly, APRA reduced the capital requirements for lending at the same time, allowing banks to lend a higher amount of money based on the same level of security.

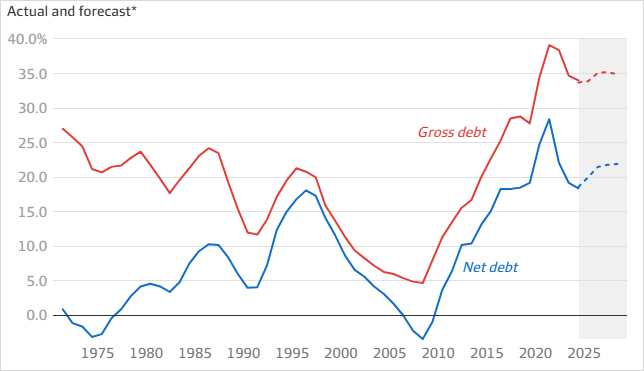

Federal government debt as a share of GDP

Source: AFR, Micheal Read

Impact on investment decisions and asset allocation.

Rising interest rates are, of course, a double-edged sword, allowing those who are saving to get a higher rate of return without taking any more unrewarded risk. There are solid returns of around 7% available in the market with first-mortgage security; accordingly, I would anticipate that we will reduce exposure to growth assets for retirees, particularly while looking for reliable income streams. There have been some concerns with the quality of lending, particularly in the US, in the private credit market, which Australia at this stage has minimal exposure to. In essence, they have been lending money against the value of software, as opposed to hard assets like property or infrastructure; if it becomes obsolete, the security they have lent against is worthless. We will continue to focus on first-mortgage security over property in Australia to support any fixed-interest investments.

Additional superannuation tax now legislated through Division 296.

This relates to additional tax on the earnings of superannuation balances above $3 million, but it does not now include unrealised capital gains. The additional tax only relates to the percentage of the total portfolio above $3 million, and there are multiple ways of mitigating this, which we will work with affected clients to achieve. For me, the saddest part of this is that it relates to the balance in your account rather than the tax deductions you receive to build your superannuation. It effectively penalises excellent investment returns and rewards mediocrity. That said, we are still very fortunate with the overall tax position for superannuation, particularly for the drawdown phase, which will now increase to a balance of $2.1 million from 1 July 2026. The Treasurer has indicated that there may be some changes to taxation in the federal budget in May, including possibly changes to capital gains tax. As I mentioned earlier, Australia has a spending problem, not a taxation problem and, quite simply, hard decisions need to be made on where we are spending our money – not on changing the tax system for people who made investment decisions, including paying stamp duty at a previous time.

Equity markets

After several days of high volatility at the commencement of the Middle East conflict, which included a spike in daily trading, markets have settled down and the VIX (volatility index) has now returned to normal settings. Importantly, dividends are being received for the interim earnings season at the moment, which will assist in helping clients meet the additional cost-of-living expenses we are currently all dealing with. There is definitely a growing level of caution in decision-making, particularly on the publicly listed markets, with many transactions now taking place via private equity where there is less transparency and liquidity, and more infrequent valuation of assets. So, in aggregate domestically, there is a focus on solid dividend-paying shares and, as there is only a finite number of companies available, the growing contributions from superannuation should act as a natural hedge against shares falling by any significant amount.

S&P/ASX 200 VIX: 1 month

Source: Market Watch

Residential property

The desire to own your own home remains one of the great goals of many Australians, and this remains unabated. Much of the recent growth has come from cities such as Adelaide, Perth and the Gold Coast, where affordability was better than Sydney. While interest rate rises may impact serviceability and access to funds, the wider issue of a lack of supply continues to force property values higher. As the principal place of residence remains exempt from capital gains tax, this continues to be a foundation strategy for financial planning for most clients. Thanks to the 3% buffer for calculating serviceability, at this stage we are not seeing a high level of defaults in the market. It will, however, make investment properties less attractive, and I think this is part of the overall strategy of lifting interest rates and threatening to change CGT legislation.

Change in dwelling values to end of February 2026

Source: Cotality

Our News

We have been keeping naturally very busy. There has been a calmness both internally and from our clients with the Middle East conflict. There is a sense that this will pass and, in fact, we have been through similar circumstances many times over the years. Do feel free to refer your family and friends to the practice, where we continue to focus on reliable advice delivered in an understandable fashion.

With our best wishes.

Tony and Fiona

ABN 42 060 673 814 • AFSL No. 407238