Greetings

This month’s newsletter primarily focuses on updating you on recent Federal Budget changes, including their likely impact on investment decisions and asset allocation.

Background – The Problem

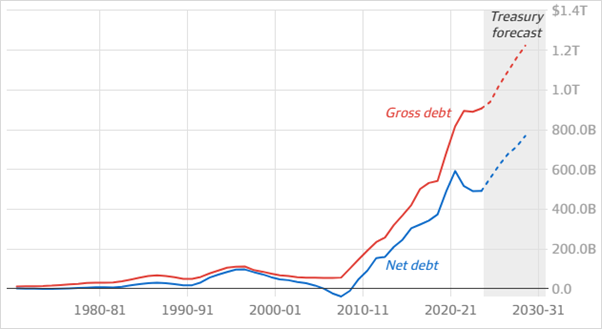

Australia has experienced several years of very poor productivity, which has led to a decline in our standard of living. At the same time, government debt has expanded to over $1 trillion, and a number of major investments, such as the NBN (which is still being held at book value), are now outdated and are being superseded by alternatives such as Starlink. In addition, NDIS costs are increasing significantly due to substantial abuse of these services.

As a result, the actual fiscal position is much worse if assets were marked to their true value, with debt potentially exceeding the value of the underlying assets.

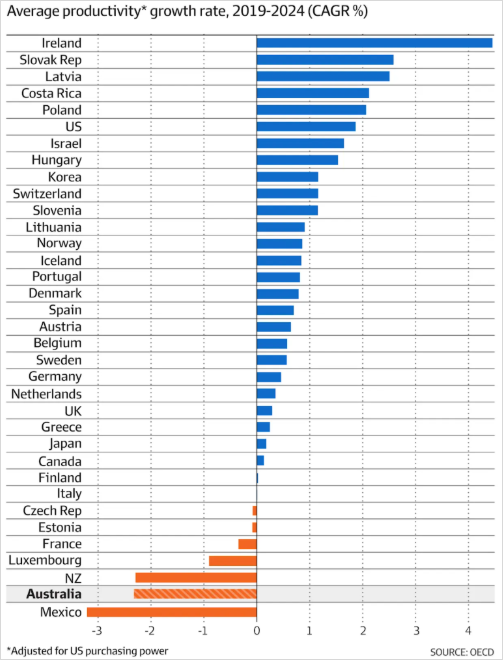

Global Productivity

Source: OECD

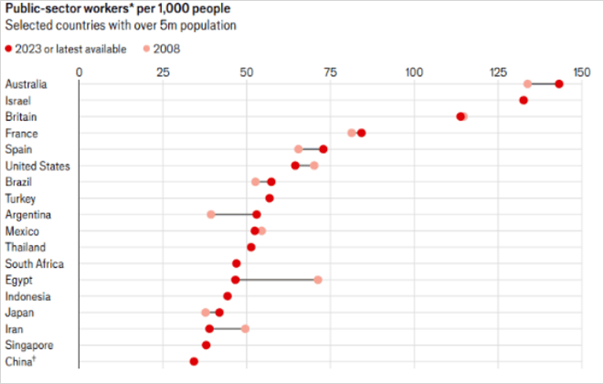

Australia also has one of the highest numbers of public servants per capita (increasing from 23.7% in 2007 to approximately 32% today, a 35% increase), occurring in the age of AI, where the private sector is reducing staffing levels.

Public Servants

Source: The Economist

Overall, the country is spending far more than it earns, with a growing portion of the Budget being allocated to interest payments on debt. At this stage, current projections indicate that government debt will continue to grow substantially for the foreseeable future, with limited public policy aimed at improving productivity.

Australia remains in a per capita recession, relying on new migrants to meet labour shortages. Unfortunately, there have not been enough homes built to accommodate this growth, resulting in a shortage of supply and increases in house prices.

Federal Government Debt

Source: Australian Financial Review

The Options

With productivity and the overall net budget position deteriorating over a number of years, this is clearly not a sustainable position going forward.

The two main tools available are:

- Fiscal policy (tax policy changes made by the government of the day), and

- Monetary policy (interest rate changes made by the RBA).

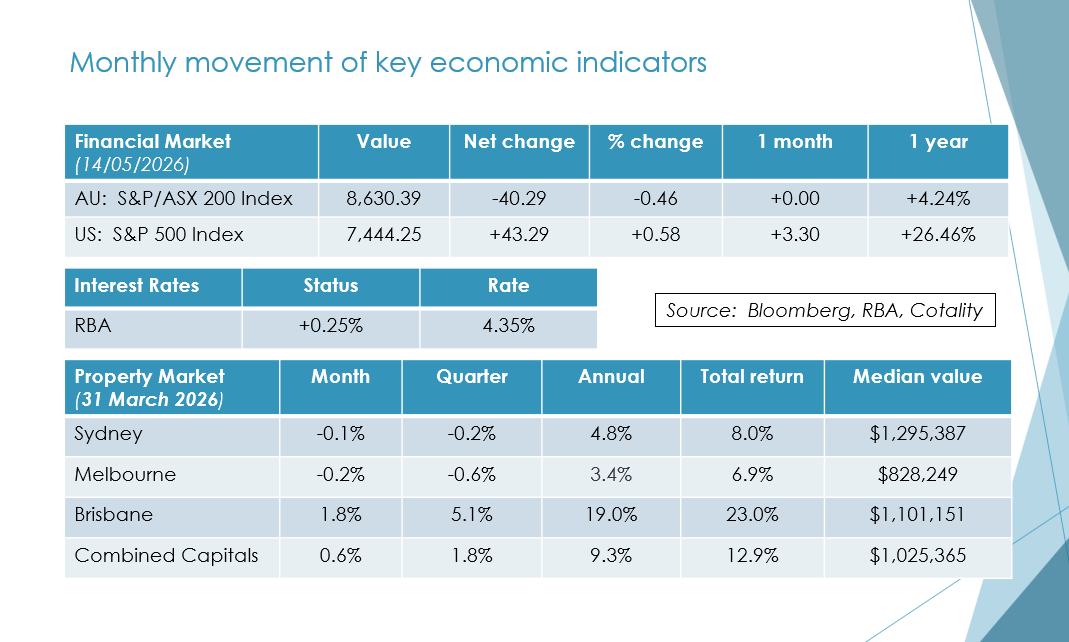

Earlier this month, the RBA lifted interest rates by 25 basis points to 4.35%, effectively returning us to the same position prior to last year’s three reductions. This contrasts with our major trading partners, including the US, and has contributed to the Australian dollar increasing from 0.63 to 0.73 USD (which also reduces the value of US equities when converted into Australian dollars).

Tax policy broadly falls into two categories:

- Direct taxes (income tax, company tax, etc.)

Australia has one of the highest direct tax burdens at 47% compared to alternative jurisdictions for Australian expats (e.g. Singapore maximum 24%, Hong Kong maximum 17%). - Indirect taxes (consumption taxes such as GST)

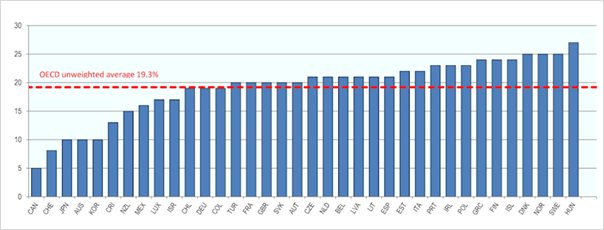

Australia relies more heavily on direct taxation and has a comparatively low GST rate. By contrast, GST/VAT rates average around 19.3% across the OECD.

Standard VAT Rates in OECD Countries, 2024

Source: OECD

The Budget Decisions all focused on direct taxation

The Budget announcements focused purely on direct taxation, with no discussion of increasing GST or implementing compensatory measures for lower-income Australians.

Changes to Capital Gains Tax (CGT)

From Budget night, future CGT calculations will be based on the pre-1999 indexation method rather than the current 50% discount applied after holding an asset for 12 months. This is a more complex calculation and is influenced as much by inflation as by the growth of the underlying asset.

This approach favours a more conservative investment strategy, focusing on higher income and lower capital growth.

A carve-out was announced for new properties to limit any reduction in supply and increases in rent. However, for buyers of new properties, any eventual sale is likely to be to an owner-occupier rather than another investor, meaning CGT will still apply at that time.

CGT is only payable upon the sale of an asset. As a result, two potential strategies may emerge:

- Selling assets after a set period (e.g. five years) to crystallise gains before they become too large, or

- Holding assets long term and passing them on to the next generation.

These rules will also apply to shares and managed funds, where smaller portions of holdings can be sold progressively over multiple tax years.

The Government has also introduced a minimum CGT rate of 30% on the net growth of an asset. Unlike the pre-1999 rules, this cannot be averaged over five years. This rate will also apply to trust distributions, irrespective of the beneficiary’s underlying income.

While existing investments will largely be grandfathered, these changes will have a significant impact on younger investors who have had less time in the market. It may also reduce the attractiveness of global equities, where other countries offer more favourable CGT regimes.

Additionally, bracket creep means that CGT realised in a single year may push investors into higher tax brackets.

The Federal Government expects these policies to add approximately 7,500 first home buyers per year (75,000 over ten years), compared with current net migration of approximately 400,000 per year.

The underlying issue remains a lack of housing supply, and these measures may discourage private investment in the property sector.

Changes to Negative Gearing

Previous attempts to remove negative gearing (including in Australia in 1985 and New Zealand in 2021) were ultimately reversed due to higher rents and reduced housing supply.

Under the proposed rules:

- Investors will no longer be able to deduct interest expenses exceeding net rental income.

- Likely responses include increasing rent, drawing on savings, or selling the property.

Budget estimates suggest rents may only increase by $2 per week, which appears optimistic based on overseas experience 10% is much more likely ($60 – $80 a week).

These changes will primarily affect individuals in their 30s and 40s with higher incomes and significant expenses, who rely on negative gearing to build wealth.

Higher-value investment properties in Sydney and Melbourne with large mortgages will be most affected. Investors may instead shift toward lower-cost, off-the-plan properties outside these areas.

Overall, this is likely to reduce housing supply, increase rents, and limit new construction. On the positive side, it may reduce pressure on the RBA to raise interest rates further.

What Has Not Changed (At This Stage)

The family home remains exempt from CGT upon sale.

Individuals can still hold up to $2 million per person in superannuation and draw a tax-free income stream from age 60 (or 65 if still working). For many Australians, this will remain a key strategy for wealth accumulation and retirement income.

There are currently no limits on franking credits from Australian shares. Combined with the CGT changes, this makes high-income, fully franked dividend-paying investments more attractive, particularly within superannuation.

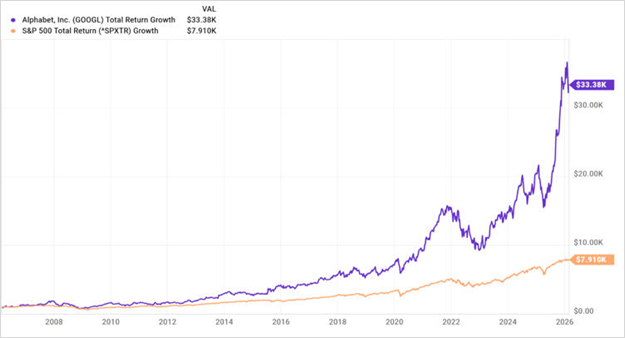

Global Shares

Despite ongoing uncertainty in the Middle East, technology companies have performed strongly, with the Nasdaq reaching new record highs.

Key highlights include:

- Alphabet (Google): up over 100% in the past 12 months

- NVIDIA: a leading provider of AI technology

- Apple: the world’s largest phone manufacturer

There is also the prospect of a future SpaceX listing, with some clients gaining exposure via the Pengana Global Private Equity Fund.

This reinforces that long-term wealth is driven by innovation and value creation, while also highlighting differences in CGT treatment between Australia and the US.

Google and S&P 500 Share Price Movement – Past Two Decades

Source: MSN, YCharts

Year‑End Planning and Asset Allocation

The coming weeks will be busy as we adjust portfolios in response to Budget changes and higher interest rates. Broadly, this will involve reducing exposure to growth assets, which face higher effective CGT, while increasing exposure to more predictable fixed-interest returns that are not subject to CGT. This approach is likely to be widely adopted and may become self-fulfilling.

Client Function – Thursday 4 June

As in previous years, we have secured a room at the Harbour View Hotel for clients visiting Vivid Sydney over the King’s Birthday long weekend. Invitations have been sent to all ongoing service agreement clients.

We look forward to seeing you there and thank you for your continued support and referrals.

Sincerely,

Tony and Fiona